Welcome to the Four Insights weekly data breakdown. Each week I’m tracking the companies, trends, and signals that matter across the ecosystems I operate in — fintech infrastructure, merchant services, lending, and AI. This is Week 9 of 2026. Let’s get into it.

Big Earnings Week: FIS, Workday, Nvidia, and CoreWeave

Four companies reporting this week that I’m watching closely, each for different reasons.

FIS reports Q4 earnings tomorrow. FIS has been a pretty flat stock, but that’s not why I care about them. They provide a window into what’s happening with U.S. merchants — transaction volumes, payment trends, and the health of the businesses we serve through both ModernTax and Clearfirm. Their report is less about the stock price and more about the signal it sends about where merchant activity is heading.

Workday is in trouble — or at least, the market thinks so. Down 7% today, down 38% year-to-date. This isn’t just a Workday story. It’s the broader question of what happens to SaaS companies when AI starts eating into their value propositions. Workday sits in HR tech, which is a space we touch through ModernTax’s service lines. The question I keep coming back to: if AI agents can handle the workflows these platforms were built to manage, what exactly are customers paying for? We’ll get into their numbers when they drop.

Nvidia reports this week too. The stock has been flat year-to-date, which is notable given the 1,200% run over the past five years and 46% gain over the trailing twelve months. The questions are starting to pile up around the sustainability of the AI infrastructure buildout — which connects directly to the last topic I’ll get to. When Nvidia reports, I’m less interested in the headline number and more interested in what they say about customer concentration and forward demand.

CoreWeave also announces this week. Same theme — who’s taking on the capital risk for this massive AI infrastructure buildout, and who’s on the hook for delivering the compute? Their numbers will tell us a lot about whether the buildout is accelerating or hitting friction.

The Viral Post: Citrini’s 2028 Global Intelligence Crisis Report

If you were on X this weekend, you probably saw it. Citrini Research dropped a research piece that’s already at 6.1 million views, 399 reposts, and climbing. Every major tech beat writer is covering it. They described it as “a scenario, not a prediction” — and said dismissing it outright “requires the kind of intellectual laziness that tends to get expensive.”

I’m not going to summarize the whole thing — you can read it on their Substack — but the parts that caught my attention are directly relevant to what we do.

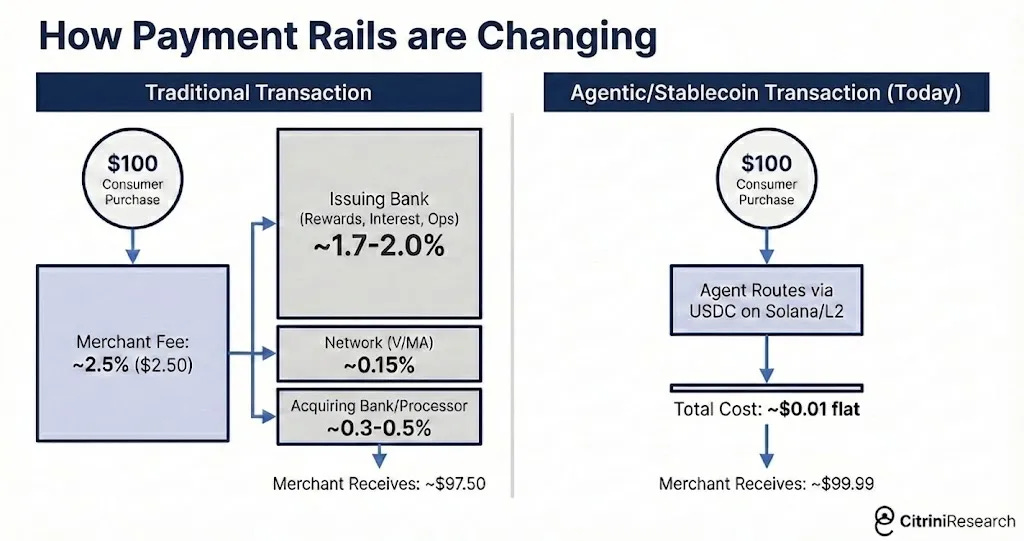

The agentic commerce thesis is real. The report breaks down a comparison that I think about constantly: traditional payment rails versus agentic stablecoin transactions. Here’s the math:

In the traditional model, a $100 purchase costs the merchant roughly $2.50 in fees. The issuing bank takes 1.7–2%, the network takes about 15 basis points, and the acquiring bank takes 3–5 bips. The merchant receives $97.50.

In the agentic stablecoin model, that same $100 gets routed by an agent via USDC on Solana or an L2. Total cost: one cent flat. The merchant receives $99.99 — with instant settlement.

This is the part that should make anyone in payments pay attention. We use Stripe for both of our businesses, and I’m always looking for ways to avoid those 2.5–3% fees. ACH helps, but it’s slow. Stablecoin rails solve for both cost and speed simultaneously.

The broader implication: this isn’t just about SaaS companies getting disrupted. This is about Amex, Stripe, Visa — companies that make their money in that 2–3% merchant fee layer — facing a fundamentally different cost structure. If agents are routing transactions and optimizing for the cheapest rail in real time, the entire payment stack gets repriced.

On Citrini themselves: I hadn’t heard of them much before this, but they’re now the #1 finance publication on Substack. They’re charging $125/month for their research, with a bundle at $2,000/month. That’s a serious content business built on the back of deep research and strong distribution. Worth studying as a model.

The 40,000-Acre Problem: AI’s Physical Constraints

This is the story that got me thinking differently this week.

The Guardian ran a piece on U.S. farmers rejecting multimillion-dollar data center bids for their land. The headline number: there’s a projected 40,000-acre deficit for data center development globally over the next five years, according to a September 2025 report from JLL. That’s double the roughly 20,000 acres currently in use.

We think about AI as this purely digital, online thing. But when you break it down to first principles, the entire AI buildout runs on three physical inputs: land, power, and water. And all three require financing and permitting — which is exactly the world I live in.

I own some rural property back where I grew up. This article actually has me doing math on whether certain parcels in the right zip codes could be positioned for this kind of development. Real estate is always about location, and data centers need specific things — power grid access, fiber connectivity, water for cooling, and local government buy-in. But the demand signal is undeniable.

This also connects back to the CoreWeave and Nvidia earnings stories. If we’re 20,000 acres short of where we need to be, and farmers are pushing back on selling, the capital requirements for the AI buildout are going to be even larger than the market is pricing in. Someone’s got to finance all of this. Someone’s got to permit it. And someone’s got to build on it.

For those of us in lending and financial services, this is a space worth watching closely.

The Week Ahead

Here’s what I’m tracking:

Tuesday: FIS Q4 earnings — watching merchant transaction data and guidance

Midweek: Workday earnings — the SaaS reckoning continues

Wednesday: Nvidia earnings — forward demand signals and customer concentration

This week: CoreWeave — infrastructure buildout velocity and capital structure

Ongoing: Citrini report fallout — watching how the agentic commerce thesis spreads through the fintech ecosystem

I’ll be breaking down each of these as they drop. If you’re in fintech, lending, payments, or just trying to understand where capital is flowing — this is the week to pay attention.

📚 Resources & Links

🔗 Follow Along

🎥 Watch the full video breakdown on my Substack.

Got thoughts on any of these? Reply to this email or hit me on X @mattaparker.

— Matt